{kind=link}

It was a difficult September for bond and stock bulls. After reiterating ad nauseum, it appears that the FOMC’s “higher for longer” message has finally gotten through. In general central banks are mostly in wait and see mode as they assess the many crosscurrents to determine whether additional tightening is needed. Uncertainties over the policy course tied the markets in knots over Q3. Yields climbed over Q3, though much of the erosion came in September, and in large part after the FOMC’s hawkish dots.

As Q4 begins, the Fed is faced with another tough choice, hold or hike. Q3 ended with a few surprises, and especially the advance indicators numbers that boosted the Q3 GDP outlook measurably to a 4.8% growth rate from 3.7% previously. That will keep the Fed, and especially the hawks, on guard. The November 1 Fed rate hike is still on the table assuming the numbers remain firm, in line with the upward revision to Q3 GDP estimate to a 4.8% rate of growth from 3.7% before Friday’s advance data release.

Real sector data has continued to surprise on the high side, while inflation has been cooling — will the strength in the economy limit further progress on reaching the 2% target?

However there is one crucial release on tap this week, tomorrow’s September nonfarm payrolls. The September nonfarm payroll report should reflect some cooling overall but still a robust labor market. It is projected with a 140k increase after gains of 187k in August, 157k in July, and 105k in June. The jobless rate should tick down to 3.7% from 3.8% in August, versus a 54-year low for the two-digit rate of 3.39% in April. Hours-worked are assumed to be flat after a 0.4% August rise, while the workweek slips to 34.3 from 34.4 in August.

Average hourly earnings are assumed to rise 0.4%, after a 0.2% gain in August, while the y/y wage gain should hold at 4.3% for a second month, with a broader downtrend reflecting the continuing return of lower-paid workers to the labor pool. Prior to the pandemic, growth in hourly earnings was gradually climbing from the 2% trough area between 2010 and 2014 to the 3%+ area until the pandemic-induced spike.

Initial and continuing claims tightened in September, while consumer confidence fell and producer sentiment improved slightly but to a still depressed level. The risk for payrolls each month is downward, both because job growth has outpaced the GDP path since 2021, and momentum for GDP growth is likely moderating.

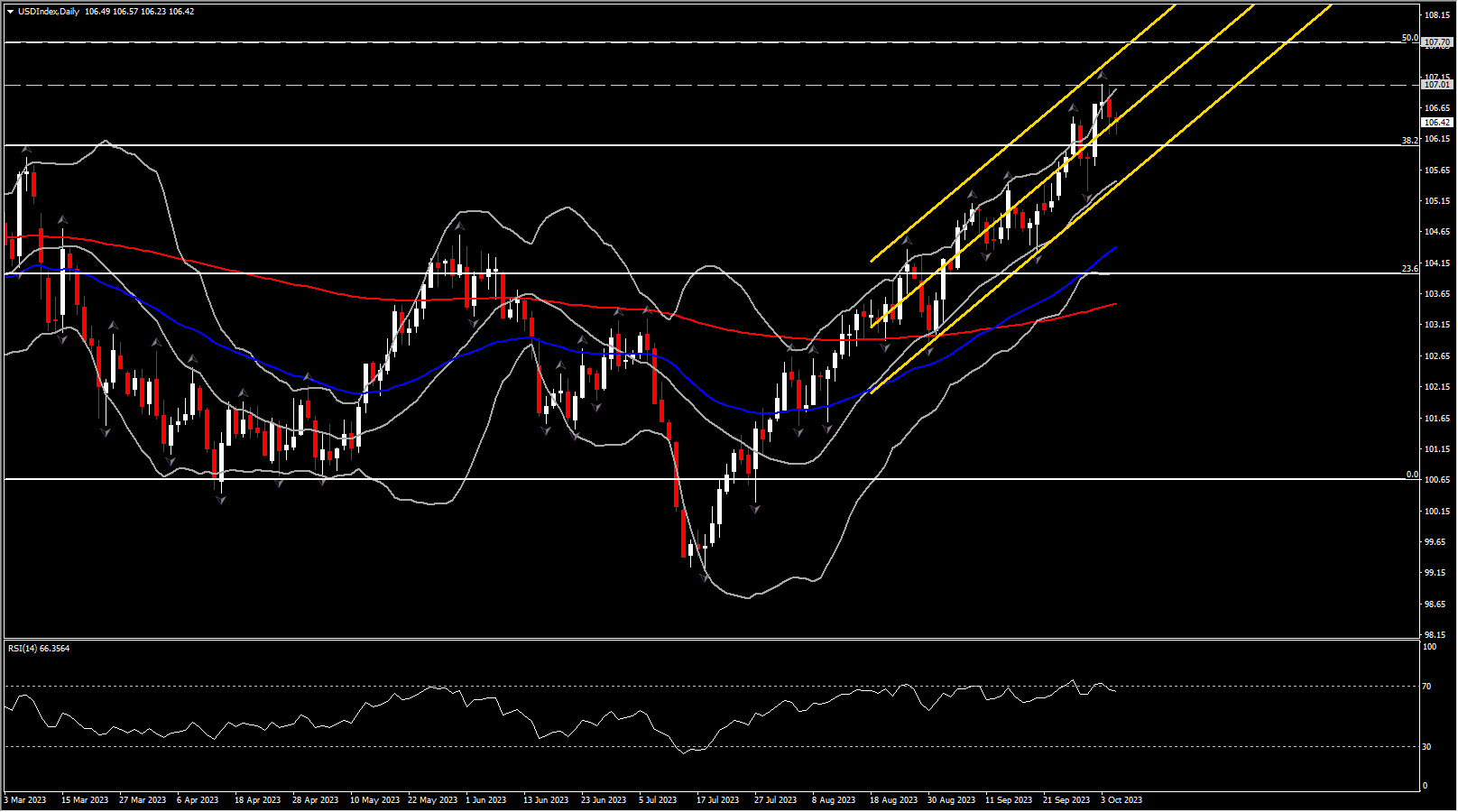

USD: Taking a Break Ahead of NFP

The USDIndex is slightly down on the day and trading at 106.20-106.60 as the focus shifts to tomorrow’s jobs report. The cautious trading today is expected to continue especially after the surprising market reaction yesterday post ADP, given their limited correlation with the actual payroll data. In fact, there seems to be an illogical inverse correlation between weak ADP numbers and strong official payroll figures.

Bonds had pared losses ahead of the ADP report and rates have extended lower after the weaker than forecast ADP encouraged dip buying and short covering. A lot of the updraft in yields was a function of a buyers’ strike.

Currently the Greenback’s correction is not attracting participants since regardless of the signs of a slowing economy, which are raising beliefs for a sidelined FOMC, there is still room for a more hawkish pricing of the US yield curve, and the US dollar’s potential for upward movement remains significant.

The USDIndex may stabilize around 106.50 today, as markets assess whether jobless claims can continue to surprise on the downside (which would be negative for bonds and positive for the Dollar). Additionally, several Federal Reserve speakers are scheduled to make remarks, most of whom are expected to express hawkish views, providing further support for potential rate hikes.

The upcoming significant milestone for the USDIndex remains the round 107. A confirmed breakout of that level could breach the 107.70 -108 range if there is a more pronounced downturn in the US bond market.

Click here to access our Economic Calendar

Andria Pichidi

Market Analyst

Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission.