The US September jobs report today exceeded expectations, with non-farm payrolls increasing by 254K compared to the 140K anticipated. The unemployment rate fell slightly to 4.1%, nearly reaching 4.0%, and the participation rate held steady at 62.7%.

Private payrolls surged by 223K, while average hourly earnings rose by 0.4% month-over-month and 4.0% year-over-year, both above forecasts.Manufacturing payrolls dropped by 7K, an improvement over prior data.

The household survey showed a gain of 430K jobs, with a notable increase in full-time employment (+631K) but a decrease in part-time jobs (-201K). The strong data diminished expectations for a Federal Reserve rate cut at the November meeting, driving the US dollar higher, but implies a more solid US economy.

With the Fed feeling that inflation is under control, if the jobs gains fill job needs, there is a chance it may not be inflationary and therefore may keep the Fed on it recalibration path.

Fed’s Goolsbee was the only Fed officisl who commented on the report, descriving it as “super,” and also highlighted the end of the port strike as additional positive news.

However, he cautioned against reacting too strongly to a single data point, emphasizing that more reports like this would increase confidence in achieving full employment. He noted that strong job numbers are likely to reflect strong GDP growth.

While the Fed is still determining the neutral interest rate, he suggested it is likely higher than zero and could fall within the 2.5-3.5% range, though there is time to figure this out. Goolsbee stressed the importance of maintaining current economic conditions, and while productivity growth could lead to a higher neutral rate, the economy would need to handle it.

He also acknowledged that broad indicators show the labor market is cooling, but rejected the notion of a “soft landing” as the economy continues to move forward.

The Fed’s ideal scenario would see unemployment between 4-4.5% and inflation around 2%, which he believes would satisfy the Fed’s goals. As more data becomes available ahead of the next Fed meeting, Goolsbee warned that external shocks could still derail efforts toward a soft landing.

For now, however, it is back to happy/giddy times. Next week the US CPI data will be released with the expectation for the headline (0.1%) and the core (0.2%) to be on the tame side once again, although the core YoY is still elevated at 3.2%. The headline YoY is expected to dip to 2.3% from 2.5%.

The news today sent stocks higher with the Dow industrial average closing at a new record high. A snapshot of the closing levels shows:

- Dow industrial average rose 341.16 points or 0.81% at 42352.75

- S&P index rose 51.13 points or 0.90% at 5751.07

- NASDAQ index rose 219.37 points or 1.22% at 18137.85

The small-cap Russell 2000 rose 32.65 points or 1.50% at 2212.79.

For the trading week, the gains were modest with the Nasdaq up 0.10%, the Dow up 0.09% and the S&P up 0.22%.

IN the US debt market, yields moved sharply higher with:

- 2 year yield: 3.928%, +21.4 basis points

- 5 year yield 3.807%, +17.4 basis points

- 10-year yield 3.967%, +11.7 basis points

- 30 year yield 4.249%, +.0 basis points

For the trading week:

- 2 year rose 36.5 basis points

- 5 year rose 30.0 basis points

- 10 year rose 21.3 basis points

- 30 year rose 14.5 basis points

Mortgage rates are back up 6.5%

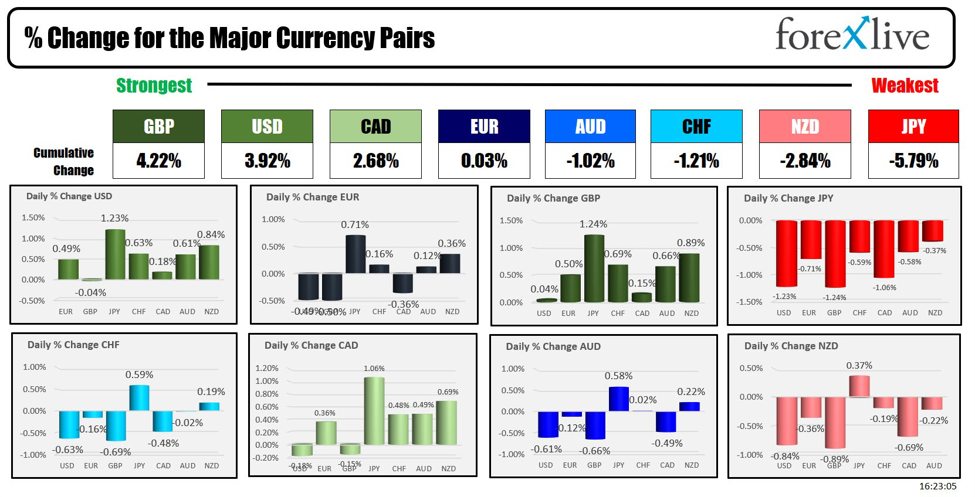

Looking at the strongest weakest of the major currencies, the GBP and the USD are the strongest while the JPY is the weakest.