Markets:

- Gold up $8 to $1941

- US 10-year yields down 14.5 bps to 4.04%

- WTI crude up $1.10 to $82.65

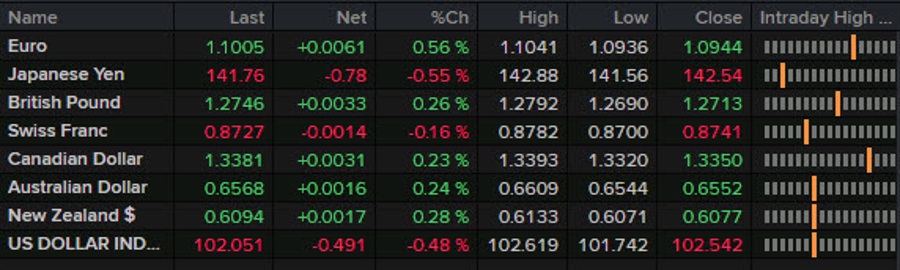

- EUR leads, CAD lags

- S&P 500 down 24 points, or -0.5%

The initial reaction to the non-farm payrolls report was to sell the dollar but then the market had a look at the higher wage data and there was a recovery. Ultimately though, a strong bid appeared for bonds and there was a growing sense that the Fed is probably done, something that Goldman Sachs reiterated in a note. Fed probabilities didn’t move much after the data but there’s only a 30% chance of another hike as the market grows confident that the economy is cooling.

I also strongly suspect that bond buyers were waiting in the weeds to buy Treasuries no matter the number. 30-year yields moved up as much as 30 bps this week but purchasers would have been scared to wade in and get blown up by another strong jobs report. So when the data was ‘good enough’ they pulled the trigger, driving yields lower and taking the dollar with it.

Initially, the dollar trade was uniform but particularly strong for the euro and pound. The latter rose to the highest levels of the week in the aftermath and USD/JPY joined in as it fell below 142.00.

Later in the day there was something of a recovery in stock markets as equities stumbled. Stocks had been strong early but faded throughout the day in a 1% reversal. With that commodity currencies were hit particularly hard and CAD ended up at the bottom of the pile despite gains for oil and gas.

The week ahead features the US CPI report and that will be another big one as the market shifts from thinking about more Fed hikes to pondering when in 2024 the cuts will begin.

Have a great weekend.